-

A Season of Echoes: Truth, History, and Unease in Fargo Season 3

Jul 7, 2026 -

MidLincoln View: The Privatization of Infrastructure

Jul 6, 2026 -

MidLincoln View: The Next Economy Is Human

Jul 6, 2026 -

MidLincoln View: When the Rules Changed

Jul 6, 2026 -

MidLincoln View: Five Civilizations, Five Ways to Allocate Capital

Jul 6, 2026 -

Introducing the Midlincoln Equities Index Atlas

Apr 12, 2026 -

Introducing the Midlincoln Bond Index Atlas

Mar 8, 2026 -

The Global Wellness Economy:

Mar 3, 2026 -

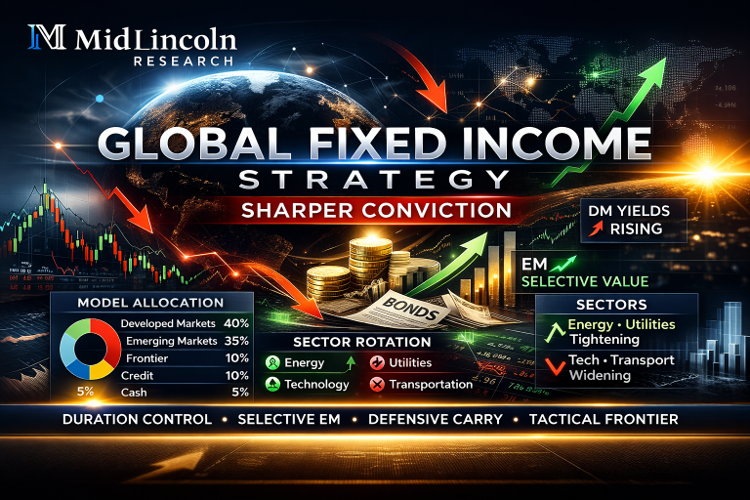

Global Fixed Income Has Entered a Dispersion Phase

Feb 24, 2026 -

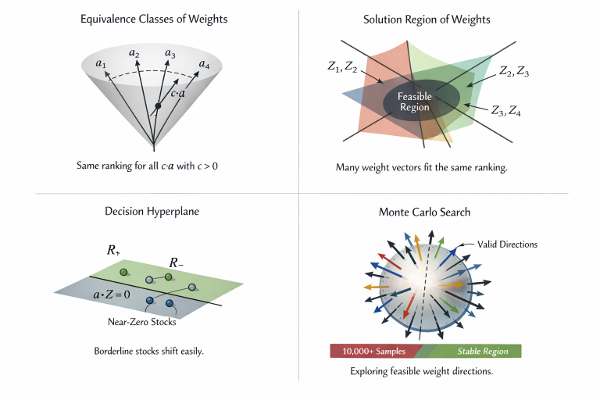

The Limits of Linear Ranking:

Feb 17, 2026 -

Ranking as Selection: From N- grams and Tokens to Equity Universes

Feb 10, 2026 -

Why Learning Factor Weights Is an Ill-Posed Inverse Problem

Feb 6, 2026 -

Ranking Before Prediction

Feb 5, 2026 -

When Power No Longer Needs Countries

Feb 2, 2026 -

Gold, Sovereignty, and the Quiet Reordering of the Monetary System

Jan 9, 2026 -

Prime Mining as Cooperative Proof-of-Work:

Dec 5, 2025 -

From Thermodynamic Markets to the Thermodynamic Economy

Nov 13, 2025 -

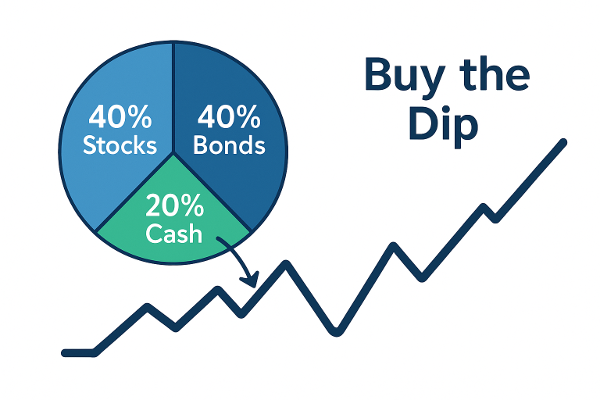

Midlincoln View: Buy the Dip 40/40/20 Portfolio Strategy

Oct 21, 2025 -

MidLincoln View - Markets, Money & AI

Oct 15, 2025 -

MidLincoln View Five Loaves, Two Fish

Oct 1, 2025