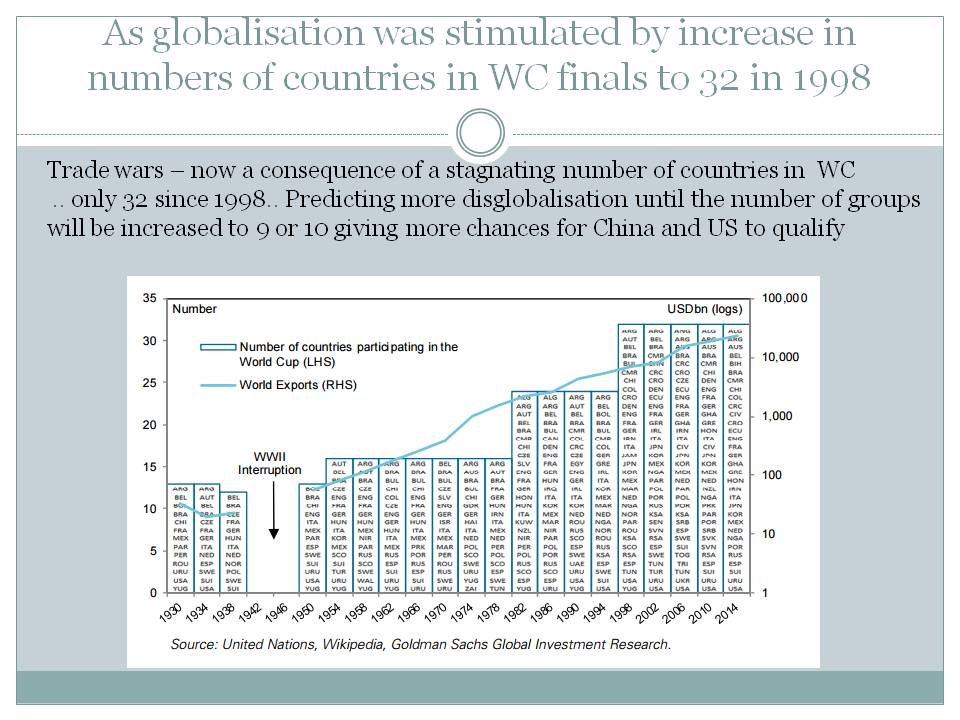

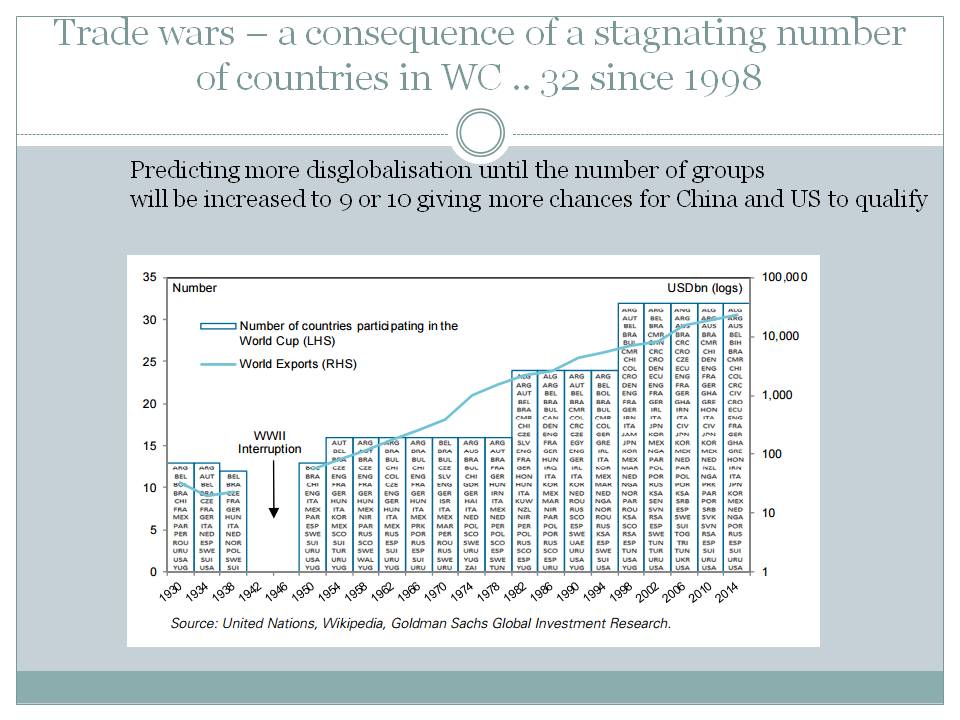

������As globalisation was stimulated by increase in numbers of countries in WC finals to 32 in 1998

Some rise in Average Goals per match would have implied higher inflation reading and possible a more robust global growth.

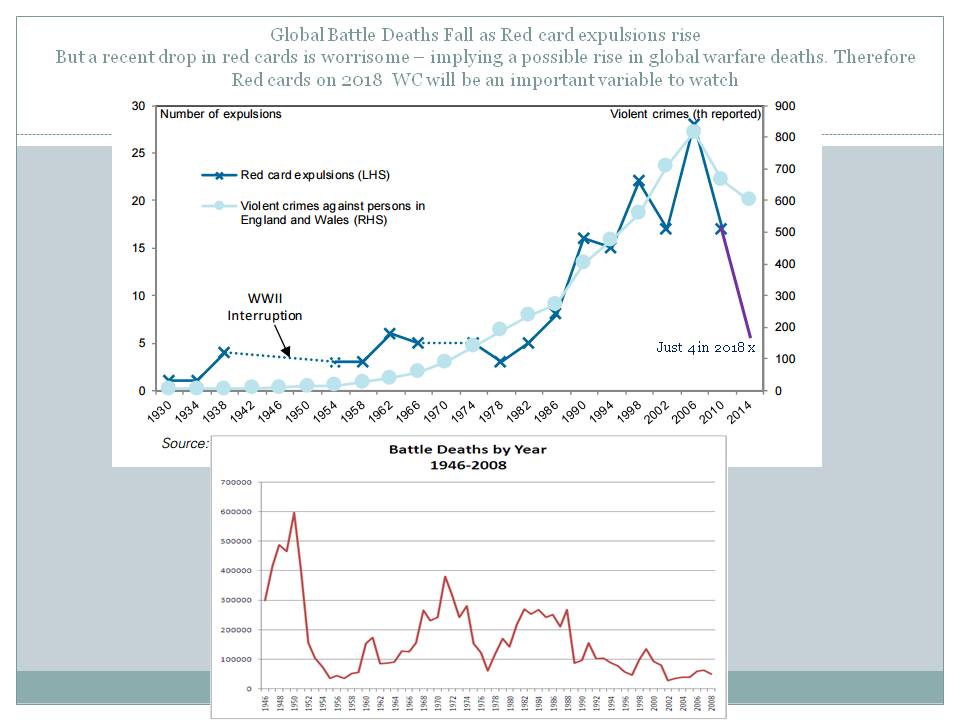

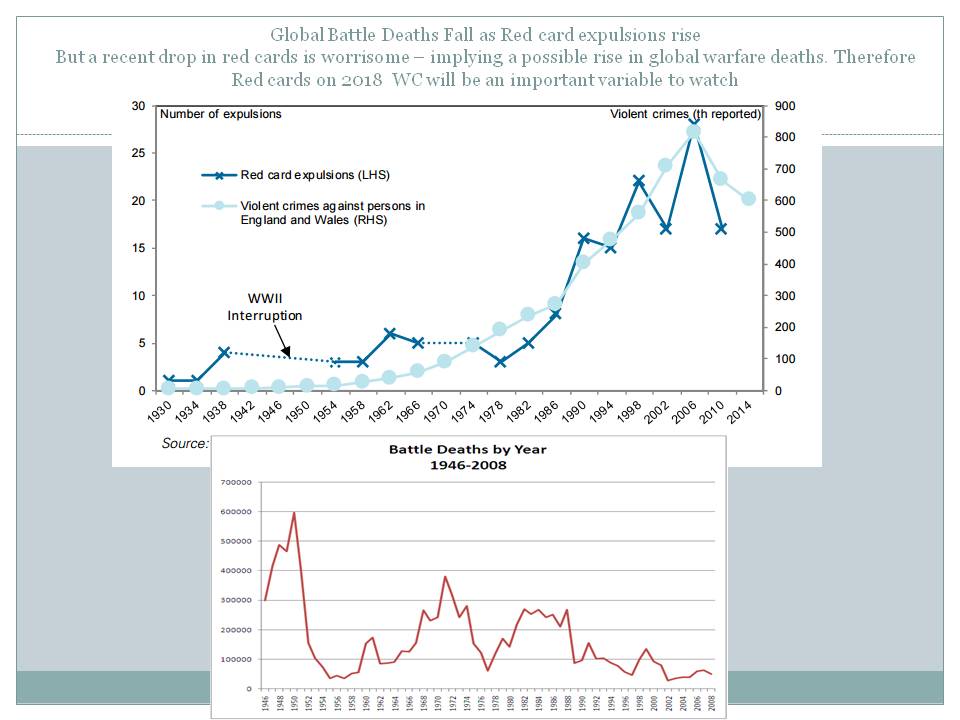

Global Battle Deaths Fall as Red card expulsions rise�

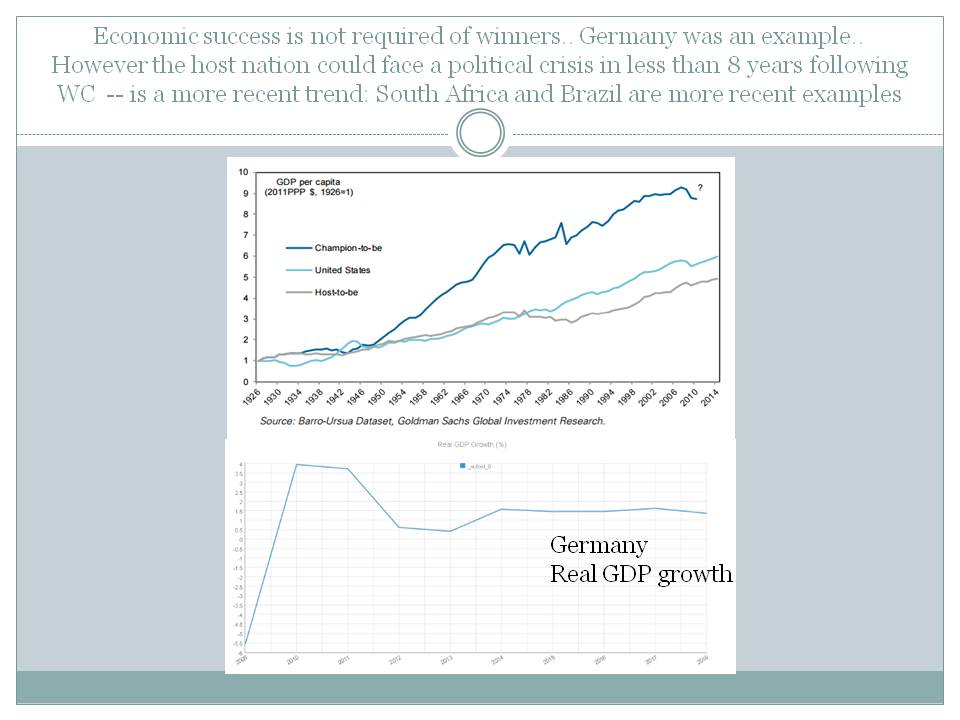

The host nation could face a political crisis in less than 8 years following WC -- is a more recent trend:

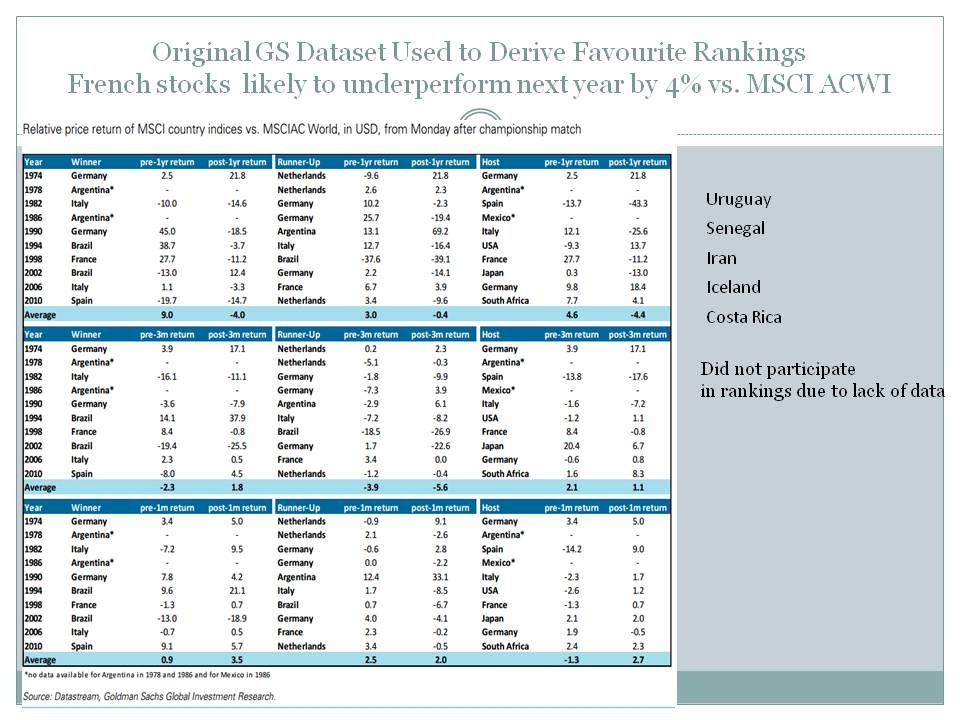

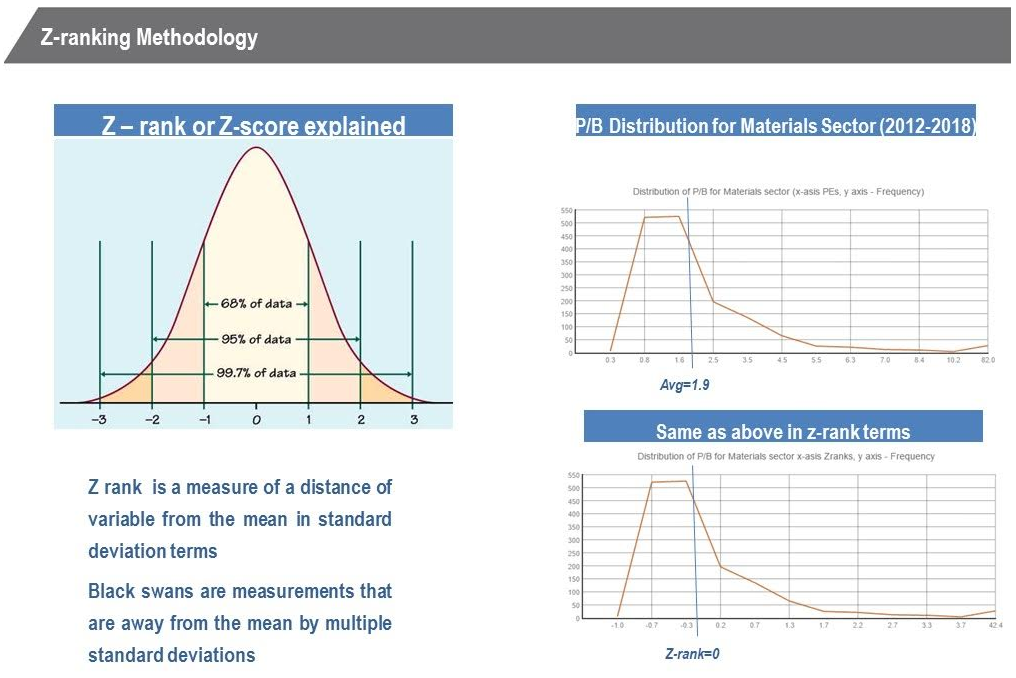

Original GS Dataset Used to Derive Favourite Rankings

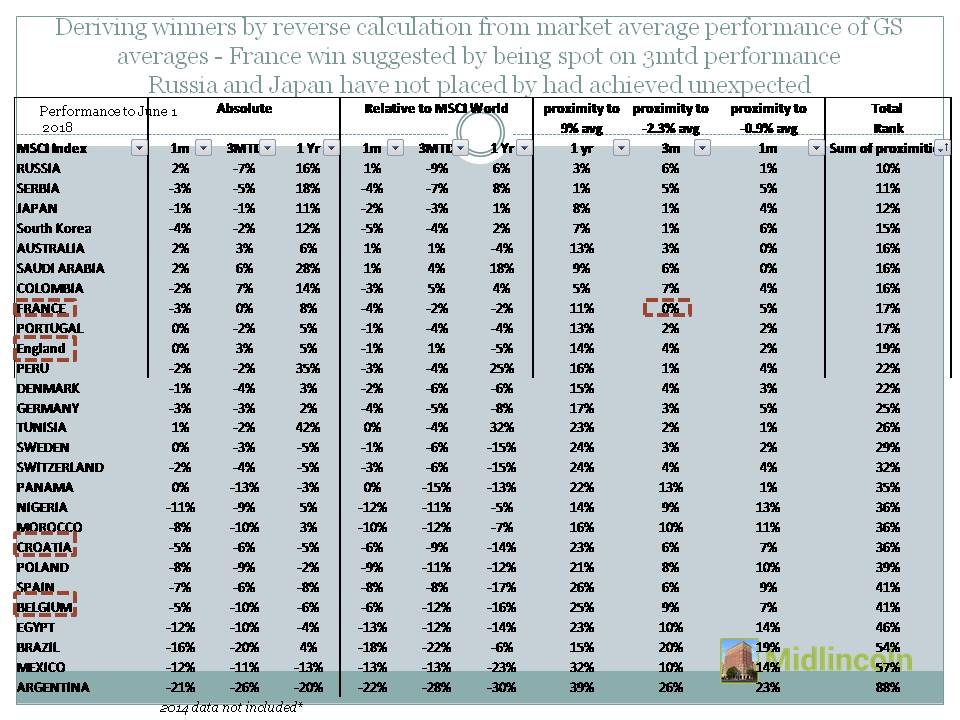

Deriving winners for WC Favourits by reverse calculation from market average performance of GS averages

Recent Strategy Chart Art

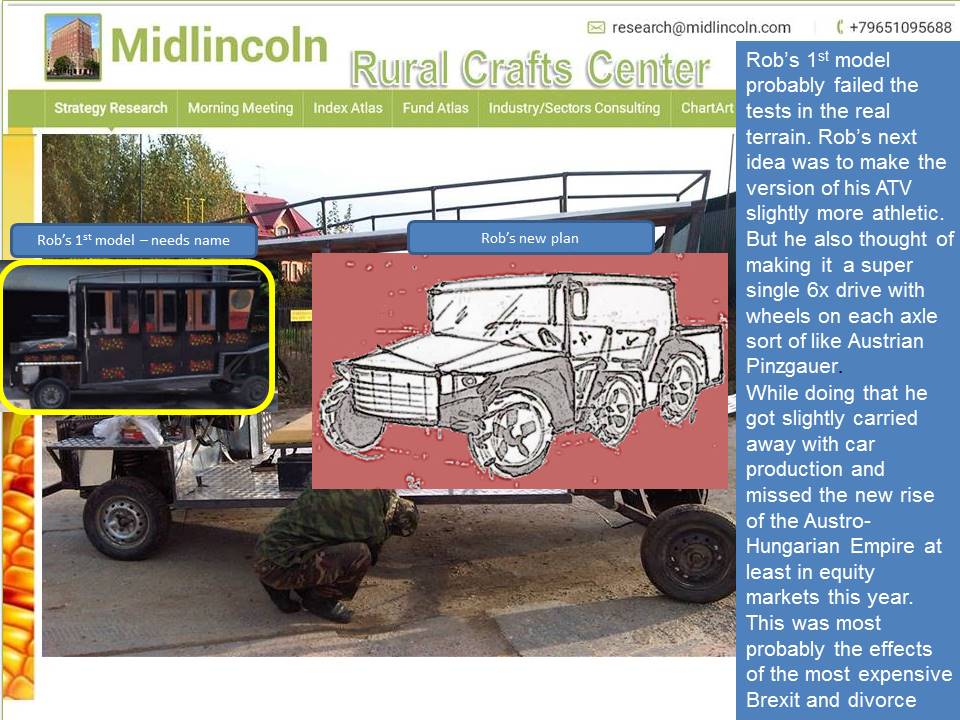

Strategy

Emerging markets bonds and equities are deteriorating. Equities are down 8% ytd and bond yields are higher by 200 to 400 btps across the board reacting to US rate hikes and higher bond yields in the US.

US markets are holding up but European equities are mostly lower.

Gold price is off its highs reacting to the same set of inputs while commodities prices are mostly lower reacting to stronger US dollar.

There is a view that deterioration is mostly done and that things will be calmer from here but there is not much supporting evidence to that.

US debt servicing is in focus on most radars and 3 to 4% interest payments on 20$trln US debt cast doubts over stability of US yields in light of economic growth which is far below 4%.

Trade wars which were last fought just before great depression don not help either and bring unpleasant memories or references.

Still it is not clear where the crisis will be coming from. The US debt doesn’t seem too big of an issue especially in light of possible negative effect on the US dollar. Trade wars seem bad but they also create opportunities.

Blockchain and internet money are far too small yet to be a significant risk.

Corporate sector is quite healthy but so it had been in 2008.

There is hope that policy makers in the US, Europe, China and emerging markets are experienced enough to sense the next danger and tackle it. But it is only a hope rooted in the past experiences of waves of QE tranches coming from one source or the other.

Lucky are those how had invested in Tunisia, Saudi Arabia domestic stocks as they are the best markets so far ytd. While less lucky are those who bought Argentina, Turkey, Poland equities as they are the worst so far YTD.

And in general - those who sold in May feel happier now.

Rarely deterioration in emerging market debt has been positive for the markets. The dividend yields which are chunky at times are not looking that attractive vs. bond yields now.

Oil price is holding up – but so it had been in 2008 right until the crash.

WC was a source of optimism and entertainment for a while – and again highlighted the rise of Europe and especially Balkans – with a link to of Austro Hungary. But now that its over the reality will be harsher.

Green shoots of next leg of globalization are seen in China rebalancing, blockchain, new silk roads and more focused of business on social development. But the rise in nationalism and dimming contextualism weigh on the negative side of globalization equation.

The strategy is quite panicky and the advice to share is to RUN but where? - Gold? Exporters? Domestics? Gold?

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Average Sovereign GEM Yields (USD)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Average Sov. Dev. Markets Yields (blended currency)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Average UST Yield

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Average Sovereign Local Currency Yields (USD)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Choose A Country

Comment

Monthly performance is between 2018-07-02 and 2018-06-01

Best global markets YTD USA +2.25%, EUROPE-6.56%, EFM ASIA-6.63%,

While worst global markets YTD EM LATIN AMERICA -14.39%, FM (FRONTIER MARKETS) -13.80%, EM (EMERGING MARKETS) -8.56%,

Best global markets last month USA-0.24%, EUROPE-3.09%, FM (FRONTIER MARKETS)-4.80%,

While worst global markets last month EFM ASIA -6.54%, EM (EMERGING MARKETS) -6.27%, EM LATIN AMERICA -5.74%,

Market wrap:US equities rose, led by the technology sector - WestpacStocks mixed as industrials rebound; dollar risesDIARY-Emerging Markets Economic Events to August 31Emerging market weakness presents opportunities in AsiaChina stocks gain despite weak US-China trade signalChina stocks gain tracking Asian shares; Hong Kong upEuropean equities open firmer to start the dayEuropean equities ahead at openOil Prices At Risk Of Economic DownturnSurprise Crude Oil Build Sends Oil Prices DownPost-rupee fall, steel prices rise againManufacturers raise steel prices for fourth time this yearTop Five Factors That May Guide Gold Prices In Near TermWhat drives the price of gold

Best last month among various countries' equity markets were TUNISIA +5.75%, KUWAIT +5.42%, TRINIDAD AND TOBAGO +3.12%, BAHRAIN +2.63%, NIGERIA +2.44%, MEXICO +2.19%, ROMANIA +1.84%, ISRAEL +1.67%, NEW ZEALAND +1.30%, BELGIUM +1.27%,

While worst last month among various countries' equity markets were ARGENTINA -23.38%, BOTSWANA -10.68%, KOREA -10.44%, THAILAND -9.53%, BRAZIL -9.53%, SOUTH AFRICA -9.14%, SINGAPORE -8.81%, INDONESIA -8.72%, PAKISTAN -8.11%, LEBANON -7.61%,

Best YTD among various country equities were TUNISIA +35.04%, SAUDI ARABIA DOMESTIC +20.21%, ZIMBABWE +15.63%, TRINIDAD AND TOBAGO +13.33%, COLOMBIA +10.21%, KENYA +9.22%, ROMANIA +5.11%, JORDAN +4.86%, ISRAEL +4.84%, FINLAND +4.74%,

While worst YTD among various country equities were ARGENTINA -47.11%, TURKEY -32.40%, MAURITIUS -25.76%, PHILIPPINES -21.89%, INDONESIA -21.35%, POLAND -20.65%, BRAZIL -19.93%, HUNGARY -18.80%, SOUTH AFRICA -18.14%, BOSNIA AND HERZEGOVINA -15.01%,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}