Oil price was down 4% in April, and is recording an 8% drop YTD and this is not including the oil price move down in the first week of May when Brent went down below 50$/bbl.

Gold on the other hand had a symmetrical move higher and is stronger by 8% ytd adding small gain in April.

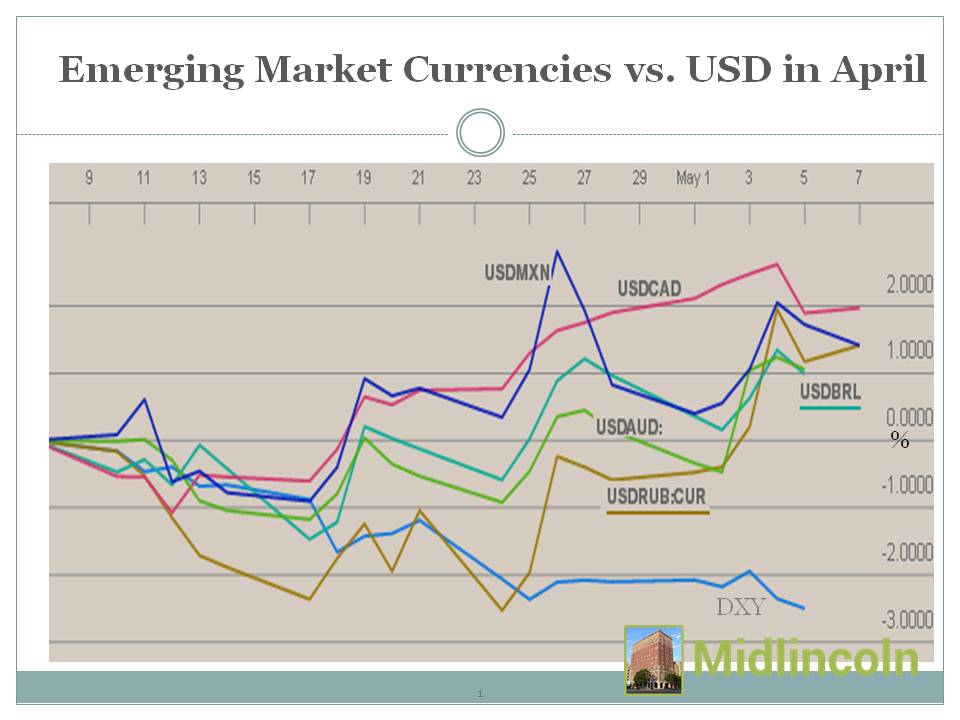

Dollar overall (DXY) has not been able to advance higher materially in April. Euro strength on the back of French election results has helped. But the buck has been drastically stronger against higher yielding currencies Russian ruble, SA rand, Aussie dollar as well as Canadian dollar as well.

Dollar strength can be especially painful for Russia local bond carry trade investors where recent profits could be mostly been surrendered to FX loses especially after the latest CBR 50btps move.

However it is difficult to call whatever is going on with a dollar, gold price, commodities prices and oil price a gloom, given that emerging markets - the key risk barometer have still been quite strong in April +2% and GEM stocks are up almost 11% YTD.

European stocks have been the leaders of the pack in April, supported by French, Austrian, Danish and Greek markets. Definitely the results of the French elections and settlement with creditors for Greek bonds have helped (Richard Ditz et al. have probably made more billions on their Greek investments).

North Korea risk has been managed so far. The only result of an escalation around North Korea so far that the developments have moved key Asian countries Japan, China and South Korea closer to the US. Yet the developments have highlighted the importance of China which is holding the upper hand in a conflict with North Korea. It is difficult to imagine the attack on North Korea similar to launched attack on Syrian air base without Chinese consent, and the later is unlikely.

Still on the back of somewhat escalated risk Asian markets have been a lot calmer in April despite the fall in the oil price from which they all (except for Indonesia and partly Malaysia) benefit. The Chinese crackdown on froth in financial markets has added to the investors' worries in Asia. It is yet unclear how further the regulator in China will go to secure financial stability which 'strategically important' to the country's economic and social development, as President Xi Jinping mentioned in a meeting of China's top politicians in the end of April. Which could result in some further tightening of the Chinese credit, but likewise it could result in more stimuli as well.

Syria has been slightly quieter in April. May started with Astana peace talks where Russia, Iran and Turkey signed an agreement to set up four safe zones in Syria. The UN described this as a promising step while the US welcome has been more cautious and several members of the opposition delegation walked out in disagreement.

Syria has been somewhat quieter in April. The plan for the "de-escalation zones" was discussed in the end of April by Trump and Putin during a telephone conversation. Putin has also been probably discussing the plans with Erdogan, who is probably cautious of Russia and US efforts in the region.

But Erdogan recently moved warmer on Russia dropping some trade restrictions while Gazprom started building the Turkish gas pipeline in Black sea.

US markets as well as Asian and emerging market stocks look a bit more vulnerable in May, as May selling likely to gather speed, given the seasonality and some ripe profits to take. But European markets look to receive some further boost from political stability.

Best last month among various countries' equity markets were SRI LANKA +14.67%, POLAND +11.47%, GREECE +11.31%, AUSTRIA +9.67%, TURKEY +9.45%, JAMAICA +9.02%, DENMARK +7.60%, BULGARIA +7.43%, PHILIPPINES +5.62%, SOUTH AFRICA +5.21%,

While worst last month among various countries' equity markets were LEBANON -8.54%, JORDAN -7.64%, TUNISIA -5.94%, PERU -4.28%, BANGLADESH -3.40%, QATAR DOMESTIC -2.63%, CANADA -2.27%, EGYPT -2.15%, QATAR -2.12%, KUWAIT -2.09%,

Best YTD among various country equities were ARGENTINA +38.33%, POLAND +31.25%, JAMAICA +27.61%, KAZAKHSTAN +25.93%, TURKEY +20.89%, ROMANIA +19.63%, AUSTRIA +19.12%, SPAIN +19.09%, INDIA +18.88%, KOREA +17.83%,

While worst YTD among various country equities were OMAN -10.19%, LEBANON -8.51%, RUSSIA -4.87%, SAUDI ARABIA DOMESTIC -3.31%, ZIMBABWE -2.98%, QATAR -2.69%, QATAR DOMESTIC -2.68%, JORDAN -2.19%, PAKISTAN -1.63%, TUNISIA -1.58%,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}